Tilbakeblikk: Juni, Q2 og første halvår: Et marked styrt av olje, AI og kraftige rotasjoner

Andre kvartal ble et av de mest dramatiske kvartalene i moderne markedshistorie, ikke nødvendigvis fordi hovedindeksene så dramatiske ut hver eneste dag, men fordi bevegelsene under overflaten var ekstreme.

På overflaten kan man oppsummere kvartalet ganske enkelt: aksjer steg kraftig, olje falt kraftig, halvledere eksploderte opp, gull og sølv falt, bitcoin fortsatte ned, og dollaren styrket seg videre. Men den egentlige historien er mer interessant. Markedet beveget seg fra frykt for stagflasjon og energisjokk til lettelse over lavere oljepris, samtidig som AI- og halvlederhandelen gikk inn i en nærmest parabolsk fase.

Dette er viktig for investorer fordi kvartalet viser hvor raskt markedet kan skifte narrativ. I Q1 var olje, inflasjon og geopolitikk den store frykten. I Q2 ble oljeprisfallet en lettelse for aksjer og renter. Samtidig tok AI-relaterte aksjer over som den viktigste risikomotoren i markedet.

Oljeprisen var den viktigste makrofaktoren

Den største enkeltforklaringen på markedsbildet i Q2 var olje. Etter et kraftig oljehopp i Q1, drevet av konflikten rundt Iran og Hormuz, falt Brent hele 38,4 prosent i andre kvartal. Det var det største kvartalsfallet siden pandemisjokket i 2020.

Dette er mer enn bare en råvarebevegelse. Olje påvirker inflasjon, sentralbankforventninger, forbrukernes kjøpekraft, selskapsmarginer og global risikovilje.

Da oljeprisen falt, ble stagflasjonsfrykten dempet. Stagflasjon betyr svakere vekst kombinert med høy inflasjon. Det er et av de vanskeligste miljøene for aksjemarkedet, fordi sentralbankene ikke uten videre kan kutte rentene for å støtte økonomien. Når oljeprisen faller kraftig, blir inflasjonsbildet mindre truende, og markedet får større rom til å prise inn vekst og inntjening.

Det var nettopp dette som skjedde i Q2. Lavere oljepris fjernet en del av det mest negative makroscenariet, og både aksjer og obligasjoner hentet seg inn etter et tøft første kvartal.

Geopolitikken skapte store svingninger

Bak oljeprisfallet lå utviklingen i Iran-konflikten. Gjennom april, mai og juni vekslet markedet mellom frykt for eskalering og håp om avtale. Trusler om angrep, usikkerhet rundt Hormuz, avlyste møter og nye forhandlingssignaler skapte kraftige bevegelser i oljeprisen.

Det avgjørende skiftet kom da markedet etter hvert begynte å prise inn en midlertidig avtale og lavere risiko for langvarig energisjokk. Da falt oljeprisen kraftig tilbake og endte juni nær nivåene før konflikten eskalerte.

Dette viser hvor viktig det er å følge geopolitikk som en markedsdriver, men også hvor raskt markedet kan gå videre når risikopremien faller. Det som én uke prises som en stor inflasjonsrisiko, kan noen uker senere bli en positiv katalysator for aksjer dersom risikoen forsvinner.

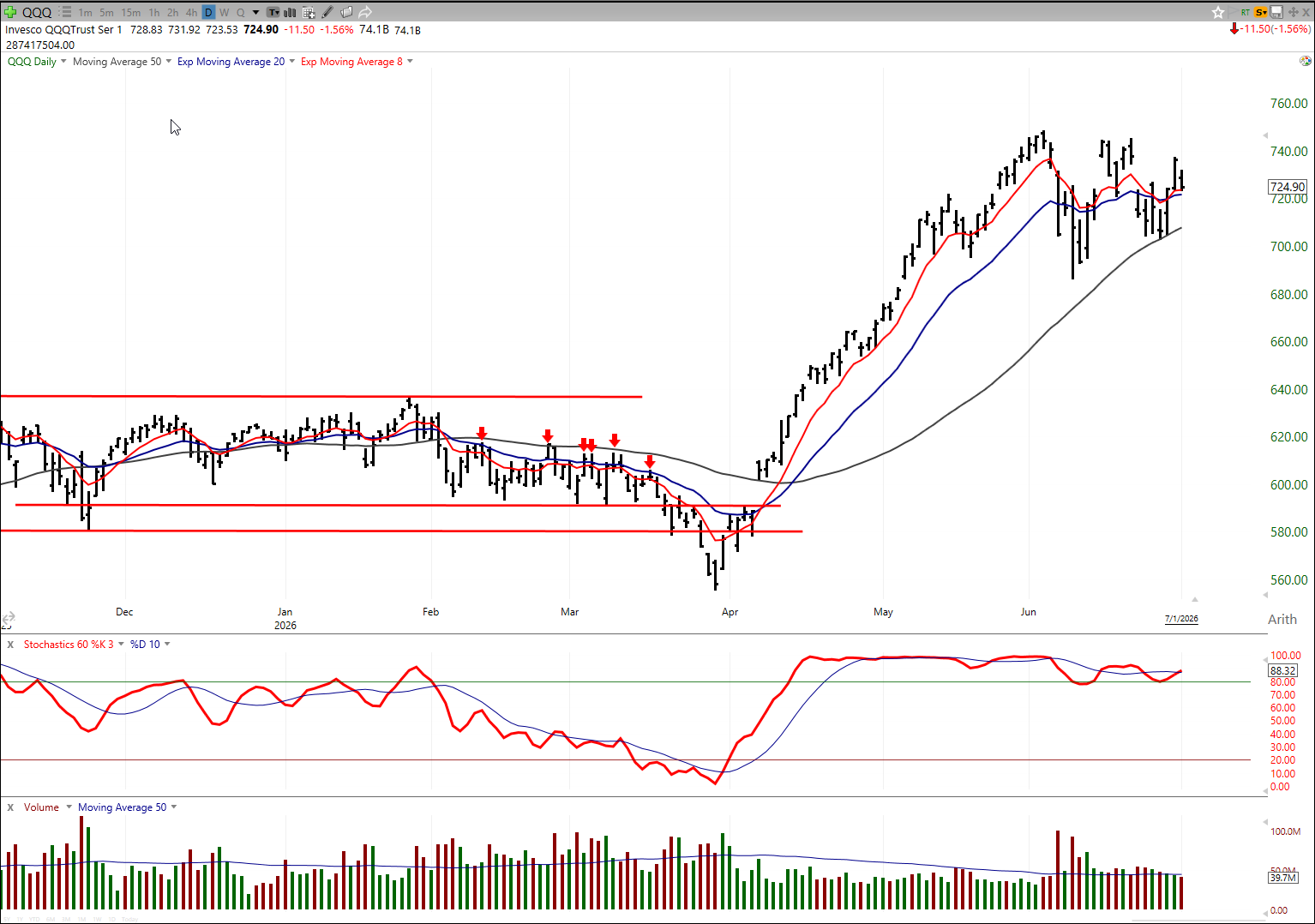

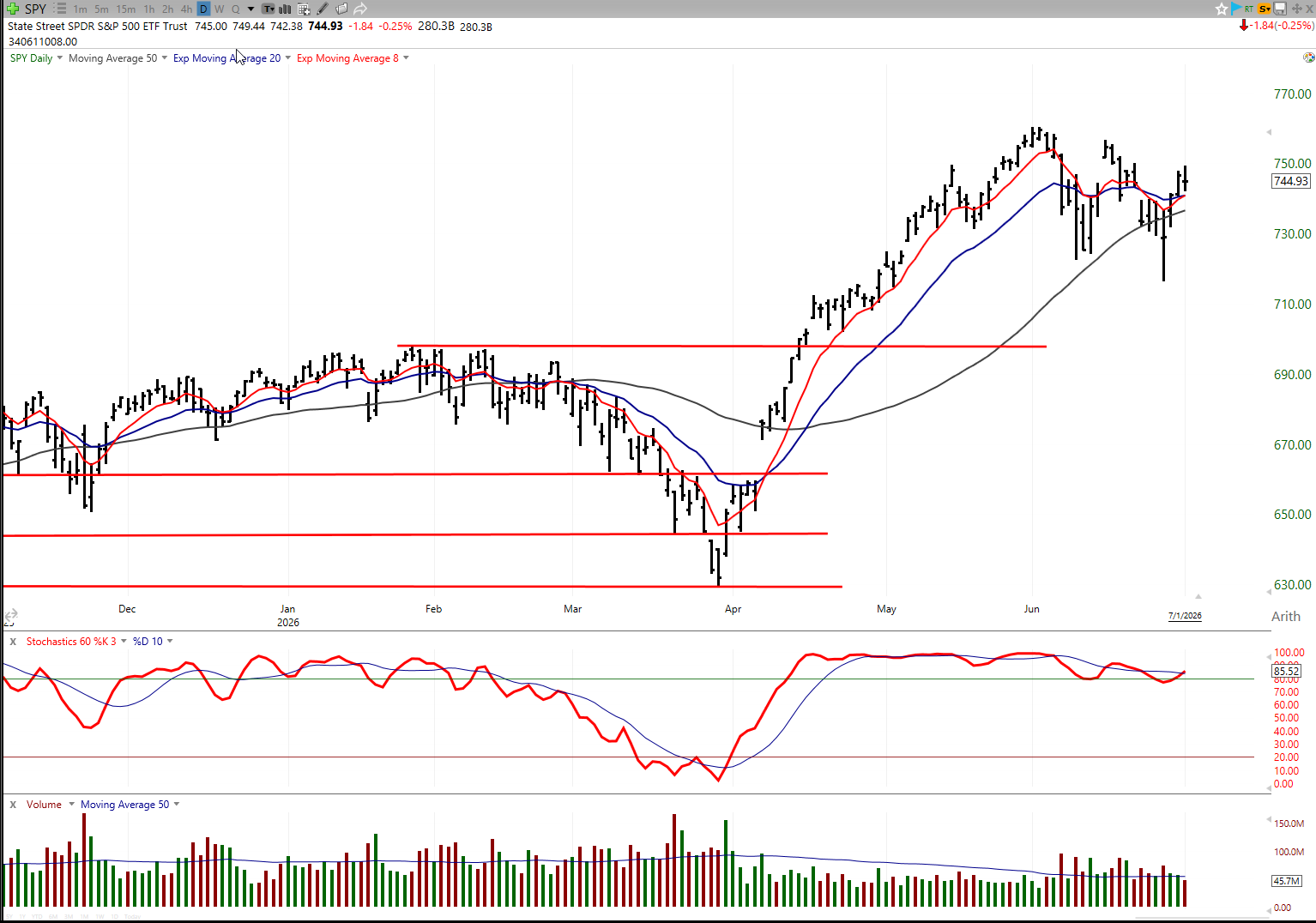

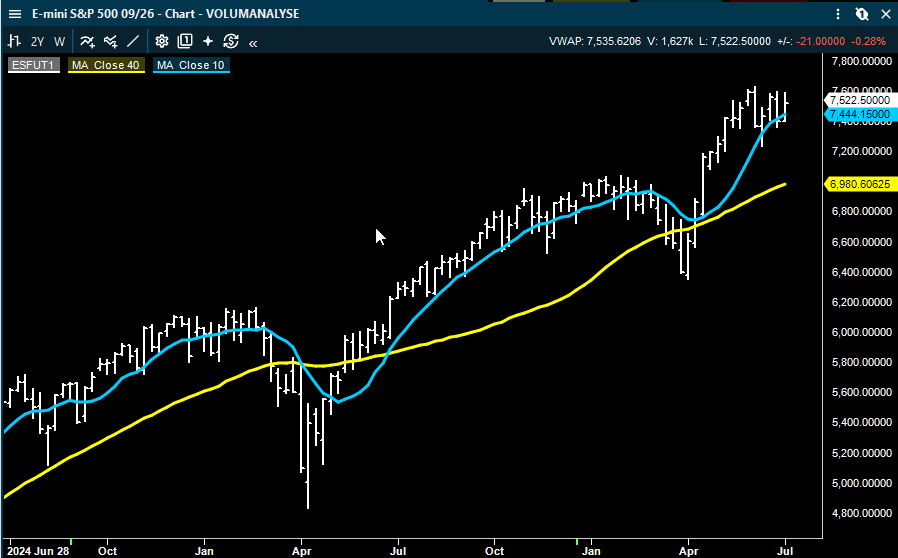

Aksjemarkedet fikk sitt beste kvartal siden 2020

S&P 500 steg 15,2 prosent i Q2. Det var det beste kvartalet siden den kraftige gjeninnhentingen etter Covid-fallet i Q2 2020. Europeiske aksjer steg også sterkt, med STOXX 600 opp 11,9 prosent.

Det er viktig å forstå hvorfor aksjemarkedet steg så kraftig. Det var ikke bare fordi alt plutselig ble bedre. Det var fordi flere negative risikofaktorer ble redusert samtidig.

Oljeprisen falt. Inflasjonsfrykten avtok. Globale nøkkeltall holdt seg bedre enn ventet. AI-investeringene fortsatte. Halvledere fikk ekstremt momentum. Og investorer som hadde vært defensive, måtte øke risiko igjen.

Når slike faktorer virker samtidig, kan aksjemarkedet bevege seg mye raskere enn funda alene skulle tilsi.

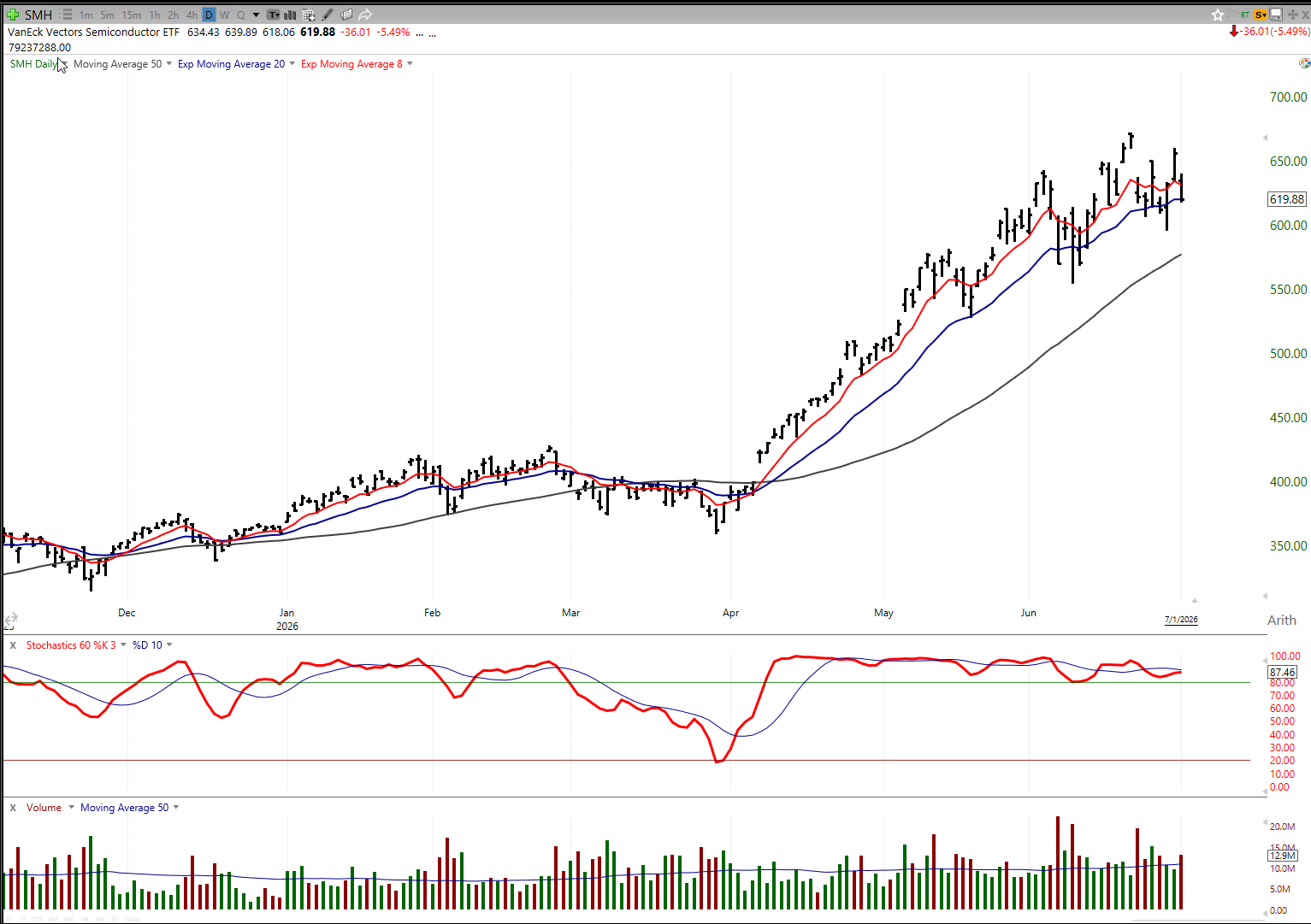

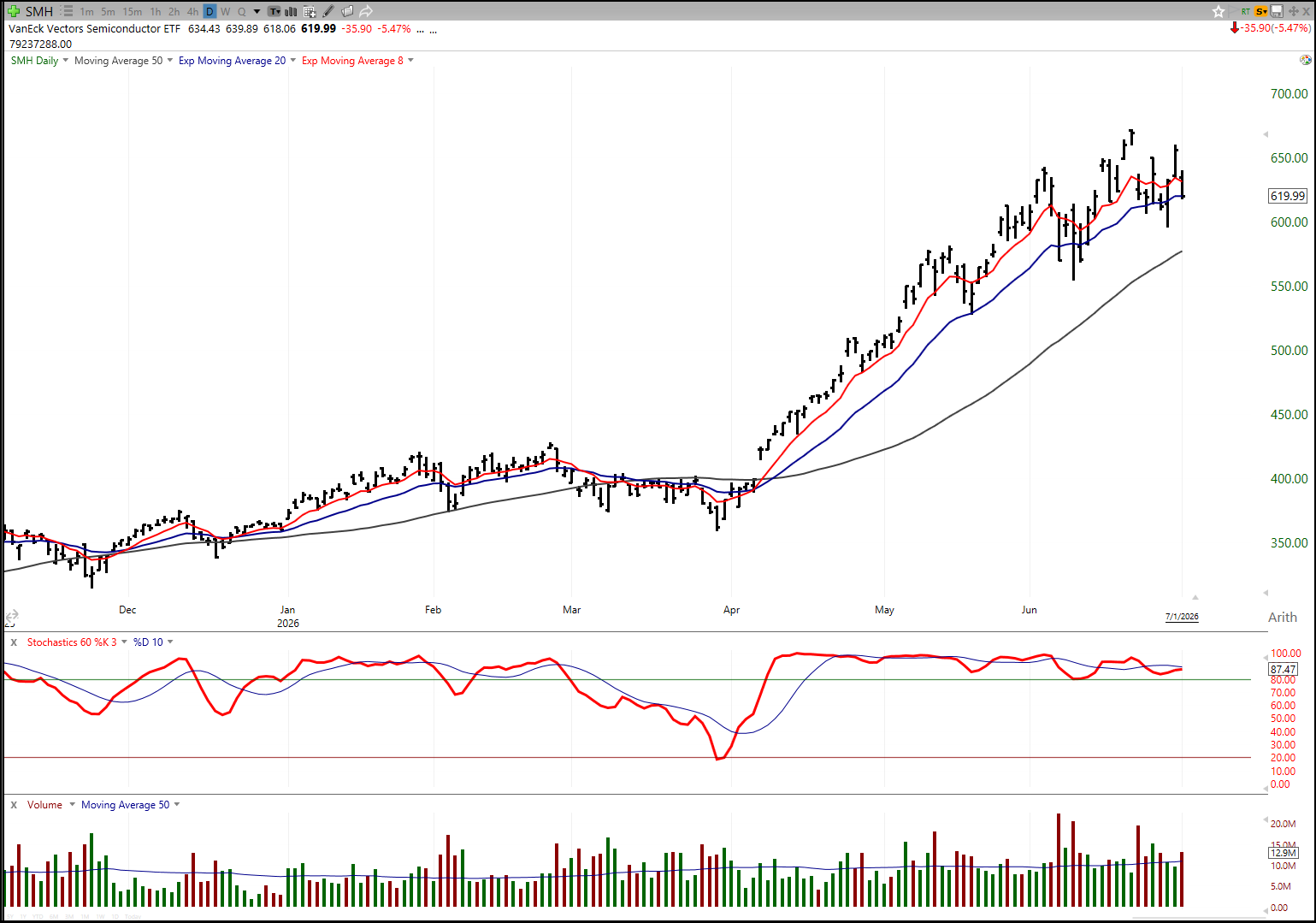

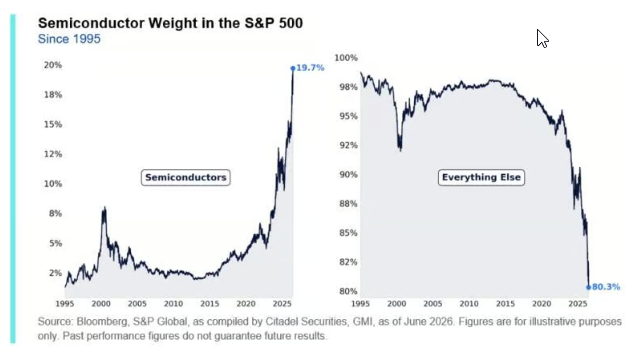

Halvledere var kvartalets store vinner

Den mest ekstreme bevegelsen kom i halvledere. Philly Semiconductor Index steg 88 prosent i Q2, den beste kvartalsavkastningen siden indeksen ble etablert tidlig på 1990-tallet. Hittil i år var indeksen opp over 100 prosent.

Dette er en enorm bevegelse. Den forteller hvor dominerende AI-handelen har blitt. Halvledere har blitt den mest direkte måten å eie AI-infrastruktur på. Hvis AI krever mer datakraft, trengs det flere chips, mer minne, mer lagring, mer nettverk og mer datasenterkapasitet.

Derfor har kapitalen strømmet inn i halvlederaksjer.

Men dette er også et risikosignal. Når en sektor stiger nesten 90 prosent på ett kvartal, blir den svært følsom for skuffelser. Da er det ikke nok at den langsiktige historien fortsatt er god. Markedet har allerede priset inn mye av den historien.

For investorer betyr dette at en sterk trend ikke automatisk er trygg. Jo sterkere og mer populær trenden blir, desto viktigere er det å følge posisjonering, sentiment og tekniske brudd.

Korea og Japan ble løftet av AI og valuta

AI-handelen stoppet ikke i USA. Sør-Koreas KOSPI steg 64,3 prosent i Q2 målt i dollarbasert totalavkastning. Det var den sterkeste kvartalsutviklingen siden fjerde kvartal 1998. Bakgrunnen var Koreas tunge eksponering mot minnebrikker, halvledere og AI-relatert teknologi.

Japan hadde også et svært sterkt kvartal. Nikkei steg 34,1 prosent i dollarbasert totalavkastning, det beste kvartalet siden første kvartal 1986.

Dette viser at AI ikke bare er en amerikansk handel. Kapitalen søker globalt etter selskaper og markeder som kan kobles til AI-verdikjeden. Korea får rollen som minne- og halvlederproxy. Japan får støtte fra svak valuta, bedre inntjening og økende internasjonal kapitalinteresse.

Men også her er det viktig å se under overflaten. Når et helt aksjemarked løftes av noen få dominerende teknologitemaer, blir markedet mer sårbart dersom samme tema snur.

Yen-fallet viser at valuta fortsatt er en nøkkelfaktor

Japan hevet renten med 25 basispunkter i juni, men yenen svekket seg likevel til det laveste nivået mot dollaren siden 1986. Det sier mye om styrken i dollaren og hvor dominerende amerikanske rente- og kapitalstrømmer fortsatt er.

Normalt skulle en renteheving støtte valutaen. Men hvis markedet samtidig priser inn en mer haukete Fed og sterkere amerikansk dollar, kan lokale rentehevinger bli overskygget.

For investorer betyr dette at valuta ikke kan ignoreres. En svak yen kan støtte japanske eksportører og løfte aksjemarkedet målt i lokal valuta, men den kan også skape bekymring for importert inflasjon og finansiell stabilitet.

Valutamarkedet forteller ofte noe om hvor kapitalen faktisk søker trygghet og avkastning.

Sentralbankene ble mer haukete

Et av de mest interessante trekkene i Q2 var at sentralbankene ble mer haukete samtidig som aksjemarkedet steg. I USA snudde markedets forventninger fra små rentekutt til prising av rentehevinger innen utgangen av året.

Det skyldtes sterkere økonomiske data. De amerikanske arbeidsmarkedsrapportene overrasket positivt, og tremånederssnittet for nye jobber steg til det høyeste nivået på to år. Den nye Fed-ledelsen signaliserte også en strammere linje, og flere FOMC-medlemmer åpnet for renteheving i 2026.

Også i Europa ble bildet mer haukete. ECB hevet renten for første gang siden 2023. Bank of Japan hevet også renten.

Dette er viktig. Aksjemarkedet steg ikke fordi sentralbankene ble mer støttende. Det steg fordi lavere oljepris og sterk AI-momentum mer enn oppveide renteuroen.

Det betyr også at markedet går inn i andre halvår med mindre rentestøtte enn mange kanskje hadde forventet.

Gull og sølv fikk en kraftig nedtur

Gull og sølv hadde vært sterke gjennom flere kvartaler, men i Q2 snudde bildet. Gull falt 14,1 prosent og sølv falt 22 prosent. Det var det største kvartalsnedgangen for begge siden Q2 2013.

Forklaringen er sammensatt. Geopolitisk risiko ble redusert, oljeprisen falt, inflasjonsfrykten avtok, og markedet begynte å prise inn Fed-hevinger. Alt dette er negativt for edle metaller.

Gull fungerer ofte som beskyttelse mot uro, inflasjon, geopolitisk risiko og fallende realrenter. Når markedet i stedet priser inn lavere geopolitisk stress og høyere renter, blir gull mindre attraktivt.

Dette viser hvor raskt en trygg havn kan miste momentum når makro narrativet endres.

Bitcoin fortsatte å falle

Bitcoin falt 14 prosent i Q2 og var ned 33,1 prosent hittil i år. Det var tredje kvartal på rad med fall, første gang siden 2020.

Dette er interessant fordi Bitcoin tidligere ofte ble sett på som en høy-beta risikoeiendel som kunne stige når risikoviljen var sterk. Men i 2026 har kapitalen i større grad søkt mot AI, halvledere, memory og aksjer med direkte inntjeningsmomentum.

Bitcoin har dermed mistet noe av oppmerksomheten til andre spekulative temaer.

Det betyr ikke nødvendigvis at Bitcoin er strukturelt ferdig, men det viser at kapitalen alltid søker den sterkeste historien. I første halvår 2026 var den historien ikke krypto, men AI-infrastruktur.

Mag 7 underpresterte – et viktig paradoks

Et av de mest fascinerende punktene er at Magnificent 7 var svakt ned hittil i år, til tross for at markedet har vært preget av AI-feber.

Dette er et viktig paradoks. Det viser at AI-handelen ikke lenger bare handler om de største teknologiselskapene. Kapitalen har rotert dypere inn i AI-verdikjeden, særlig halvledere, memory og asiatisk teknologi.

Markedet skiller i økende grad mellom dem som finansierer AI-utbyggingen, og dem som får ordrene.

De store plattformselskapene må bruke enorme beløp på capex. Leverandørene får inntektene. Derfor kan AI være en positiv historie for chipaksjer samtidig som enkelte store teknologiselskaper møter mer kritiske spørsmål om fri kontantstrøm og avkastning på investeringene.

Dette er et av de viktigste signalene fra første halvår.

Q2 var ikke et bredt marked – det var et rotasjonsmarked

Når man ser på tallene samlet, var Q2 ikke bare et sterkt aksjekvartal. Det var et kvartal med ekstrem rotasjon.

Olje falt kraftig. Halvledere eksploderte. Korea og Japan steg voldsomt. Gull, sølv og Bitcoin falt. Dollaren styrket seg. Obligasjoner hentet seg noe inn. Mag-7 underpresterte relativt til AI-temaet.

Dette viser at det ikke holder å si at «markedet steg». Det riktige er å si at kapitalen flyttet seg kraftig mellom temaer.

· Ut av oljeinflasjonsfrykt.

· Ut av edle metaller.

· Ut av krypto.

· Inn i AI-infrastruktur.

· Inn i halvledere.

· Inn i Korea og Japan.

· Inn i aksjer som nyter godt av lavere energirisiko og sterkere global risikovilje.

Hvorfor dette er viktig for investorer

For investorer er lærdommen fra Q2 svært viktig. Markedet kan endre karakter raskt. Det som er en vinner i ett kvartal, kan bli en taper i neste. Og det som ser ut som en bred aksjeoppgang, kan i realiteten være drevet av noen få ekstremt sterke temaer.

Dersom man bare ser på hovedindeksen, går man glipp av mye av informasjonen. S&P 500 opp 15 prosent sier noe om retningen. Men det sier ikke nok om hva som faktisk driver markedet.

Det som virkelig betyr noe, er å forstå hvilke aktiva som leder, hvilke som faller, hvilke narrativer som mister fokus, og hvor kapitalen flytter seg.

I Q2 var svaret tydelig: lavere oljepris fjernet stagflasjonsfrykt, mens AI og halvledere tok over som den dominerende risikodriveren.

Relevans for Oslo Børs

Dette er også relevant for Oslo Børs. Norge er et lite, åpent og sektorpreget marked. Olje, shipping, sjømat, industri og råvarer påvirkes direkte eller indirekte av global kapitalflyt.

Når oljeprisen faller 38 prosent på et kvartal, er det ikke bare en global makrohistorie. Det påvirker energiaksjer, oljeservice, inflasjonsforventninger og sentimentet rundt sykliske selskaper.

Når AI og halvledere leder global risikovilje, kan det støtte internasjonale aksjemarkeder, men samtidig trekke kapital bort fra mer tradisjonelle sektorer. Når dollaren styrker seg og yenen svekkes, påvirker det råvarer, valutaflyt og konkurranseevne.

For norske investorer betyr dette at man ikke kan analysere Oslo Børs isolert. Kapitalen beveger seg globalt. Når store internasjonale temaer endres, får det også konsekvenser for norske sektorer.

Hva bør følges i andre halvår?

· Det første man bør følge er oljeprisen. Brent falt kraftig i Q2, men var fortsatt opp nær 20 prosent hittil i år. Hvis oljeprisen igjen begynner å stige på geopolitikk eller tilbudsrisiko, kan inflasjonsfrykten komme tilbake.

· Det andre er halvlederne. Etter en ekstrem oppgang er sektoren både den viktigste lederen og den største sårbarheten. Hvis halvledere fortsetter å stige, kan AI-handelen holde markedet oppe. Hvis sektoren snur, kan det ramme global risikovilje.

· Det tredje er rentemarkedet. Markedet har gått fra å prise kutt til å prise hevinger. Hvis rentene fortsetter opp, kan høyt prisede vekstaksjer bli mer utsatt.

· Det fjerde er dollaren. En sterk dollar kan presse råvarer, EM, global likviditet og selskaper med høy dollargjeld.

· Det femte er bredden i aksjemarkedet. Dersom oppgangen fortsatt bare drives av AI og halvledere, blir markedet mer sårbart. Dersom flere sektorer begynner å delta, blir oppgangen mer robust.

Konklusjon

Q2 var et kvartal hvor markedet gikk fra stagflasjonsfrykt til AI-eufori. Lavere oljepris fjernet mye av inflasjonspresset, og det ga aksjer og obligasjoner rom til å hente seg inn. Samtidig eksploderte halvlederaksjer, Korea og Japan, drevet av AI, memory og teknologioptimisme.

Men under overflaten var bildet langt mer selektivt enn hovedindeksene antyder. Gull, sølv, Bitcoin og olje falt kraftig. Mag-7 underpresterte til tross for AI-feberen, og ble brukt til å finansiere andre momentumcases. Dollaren styrket seg videre, og sentralbankene ble mer haukete.

Dette gjør markedet mer sammensatt. Det er ikke et enkelt bullmarked hvor alt stiger sammen. Det er et marked hvor kapitalen roterer kraftig mellom temaer.

Den viktigste lærdommen er at investorer må forstå hva som faktisk driver markedet. I Q2 var det ikke bare bedre stemning. Det var et dramatisk fall i oljeprisen, en kraftig lettelse i stagflasjonsfrykten og en historisk ekstrem reprising av halvleder- og AI-infrastrukturaksjer.

For andre halvår blir spørsmålet om denne kombinasjonen kan fortsette. Hvis olje holder seg lav, inntjeningen holder seg oppe og AI-investeringene fortsetter, kan aksjemarkedet fortsatt få støtte. Men etter et kvartal med så ekstreme bevegelser, er fallhøyden også større dersom noen av de viktigste forutsetningene svikter.

Markedet går derfor inn i andre halvår med sterk momentum, men også med større risiko for rotasjon, gevinstsikring og høyere volatilitet.

Kilde: Deutsche Bank / Jim Reid

DISCLAIMER

Denne analysen er kun et utdannings- og treningsverktøy i teknisk analyse, og må ikke tolkes som en individuell anbefaling om handel i finansielle instrumenter. Point & Figure-analysen genererer kjøps- og salgssignaler utelukkende basert på en modell, der signalene beregnes fra kolonner og formasjoners bredde. I chartene fremstår disse som kjøp og salg, men dette er ikke anbefalinger fra Inside Oslo Børs – de er kun resultatet av en objektiv, regelbasert metode. Analysen er uavhengig av tid og fullstendig modellbasert. Innholdet i denne rapporten er kun ment som generell informasjon og opplæring innen teknisk analyse. Eventuelle referanser til kjøp, salg, kursmål eller signaler gjenspeiler objektive modeller som Point & Figure, og skal ikke oppfattes som personlig investeringsråd eller en anbefaling om kjøp eller salg. Taktisk Inside driver ikke porteføljeforvaltning, investeringsrådgivning eller ordreformidling, og omfattes derfor ikke av konsesjonspliktig virksomhet etter verdipapirhandelloven. Investeringer i verdipapirer innebærer alltid risiko, og den enkelte investor er selv ansvarlig for sine beslutninger. Historiske signaler eller modellberegninger er ingen garanti for fremtidig utvikling. Inside Børs og INSIDE TV er redaksjonelle medier. Ansvarlig redaktør: Roger Kristiansen. Alt innhold er analyse og kommentarer, ikke personlig investeringsrådgivning.

Ansvarsfraskrivelse:

Denne teksten er utarbeidet som generell markedsinformasjon og er ikke å anse som investeringsråd. Vurderingene er basert på offentlig tilgjengelig informasjon, tekniske og fundamentale betraktninger, og kan endres uten varsel. Historisk utvikling er ingen garanti for fremtidig avkastning.