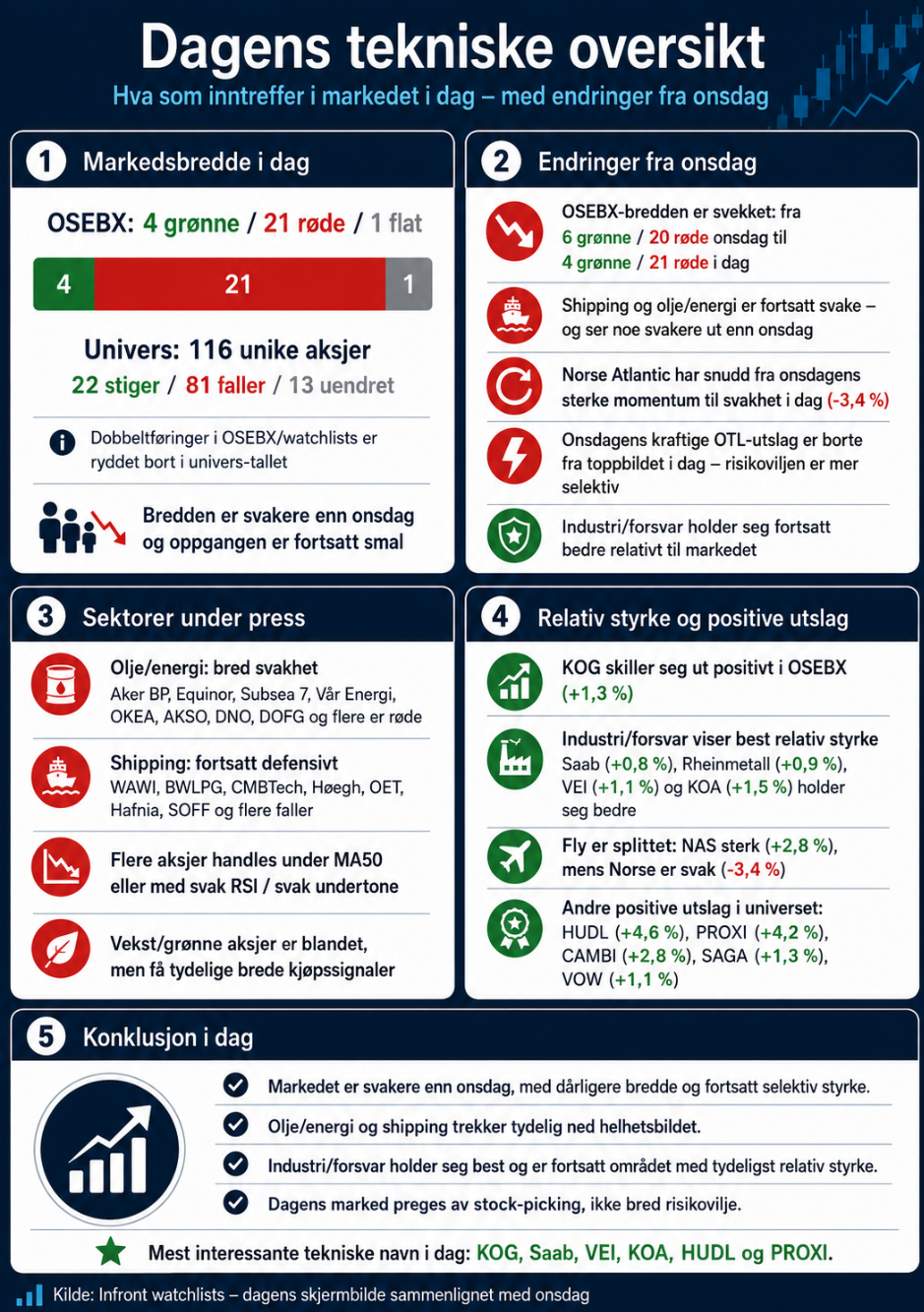

AI løfter markedet igjen, men under overflaten øker sårbarheten

Den korte børsuken endte med en kraftig oppgang inn mot fredagens helligdag og opsjonsforfall på Wall Street. Igjen var det AI som drev markedet. Det var ingen åpenbar ny enkeltkatalysator, men investorene kom tilbake til de samme temaene som har dominert lenge: halvledere, minnebrikker, strøm, AI-infrastruktur og kapasitetsbegrensninger.

Dette er et viktig signal i seg selv. Når markedet ikke trenger en stor nyhet for å løfte AI-relaterte aksjer videre, forteller det at investorene fortsatt har sterk vilje til å kjøpe korreksjoner i de ledende temaene. Den underliggende psykologien er fortsatt preget av frykten for å bli stående utenfor AI-oppturen.

Samtidig er bildet mer komplisert enn indeksene alene viser. Flere AI-relaterte kurver og temaer satte nye topper, mens S&P 500 uten AI falt. Det betyr at markedet fortsatt er sterkt avhengig av ett dominerende tema. Når AI stiger, ser markedet sterkt ut. Når AI svekkes, blir den svake bredden i markedet raskt visualisert.

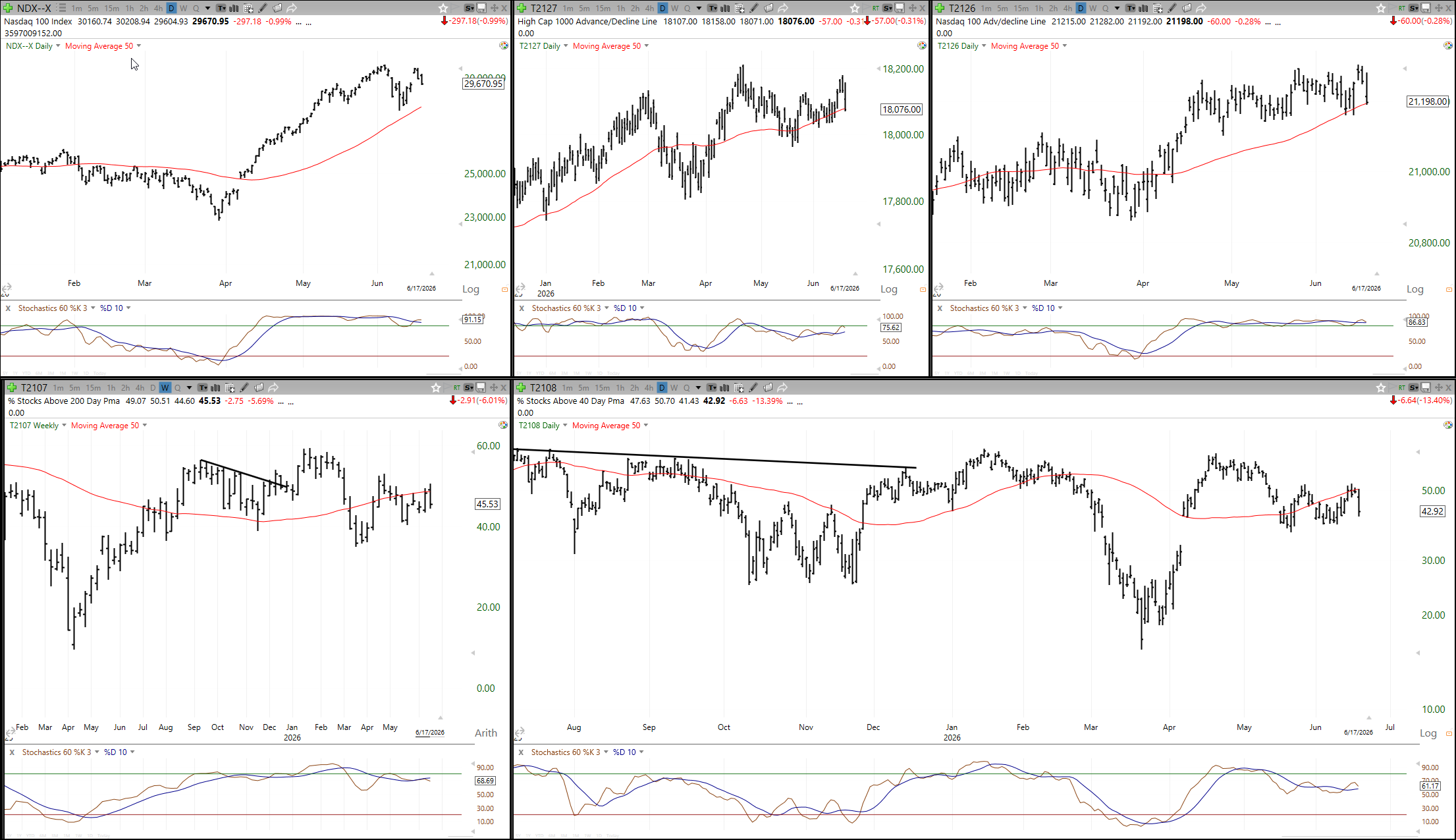

Oppgangen er fortsatt smal

Det mest interessante i markedsbildet er forskjellen mellom AI og resten av markedet. Robots & Automation, Memory og AI Semis satte nye høyder, mens S&P 500 ex-AI sluttet lavere.

Dette er klassisk smal bredde. Hovedindeksen kan se sterk ut, men oppgangen drives av en begrenset gruppe aksjer og temaer. Teknisk sett er slike markeder mer sårbare enn brede oppganger, fordi stadig mer av indeksutviklingen avhenger av at de samme lederne fortsetter å stige.

I en sunn og bred oppgang deltar flere sektorer. Kapitalen sprer seg til industri, finans, forbruk, small caps og sykliske aksjer. I dagens bilde er det fortsatt AI-komplekset som trekker mest. Det betyr ikke at oppgangen må stoppe, men det betyr at markedet har mindre sikkerhetsmargin dersom AI-momentumet svekkes.

Dette er særlig viktig fordi mange investorer allerede er tungt posisjonert i de samme AI-temaene. Når en trade blir både stor, populær og indeksviktig, kan små skuffelser gi store utslag.

Geopolitisk momentum har stoppet opp

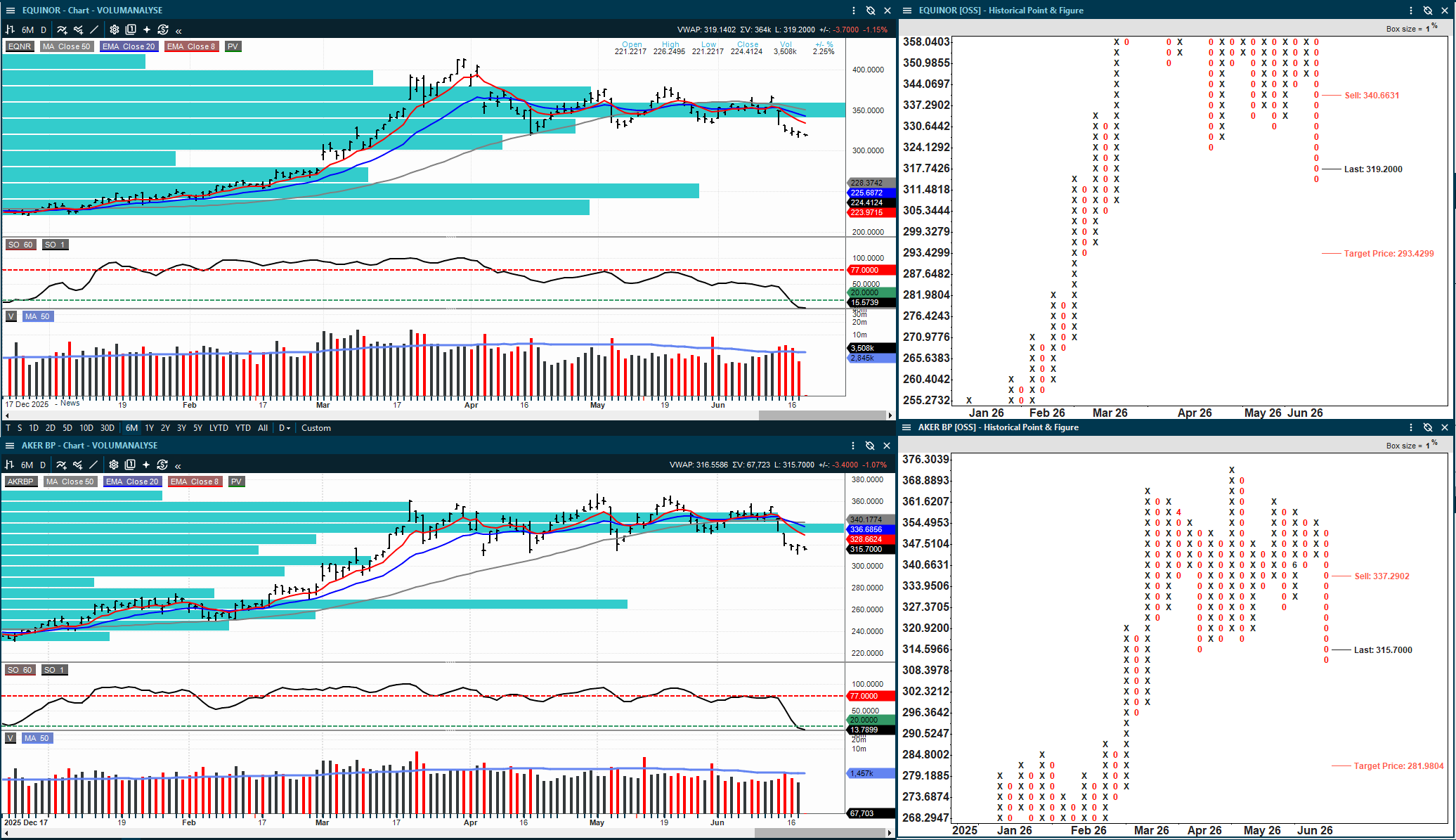

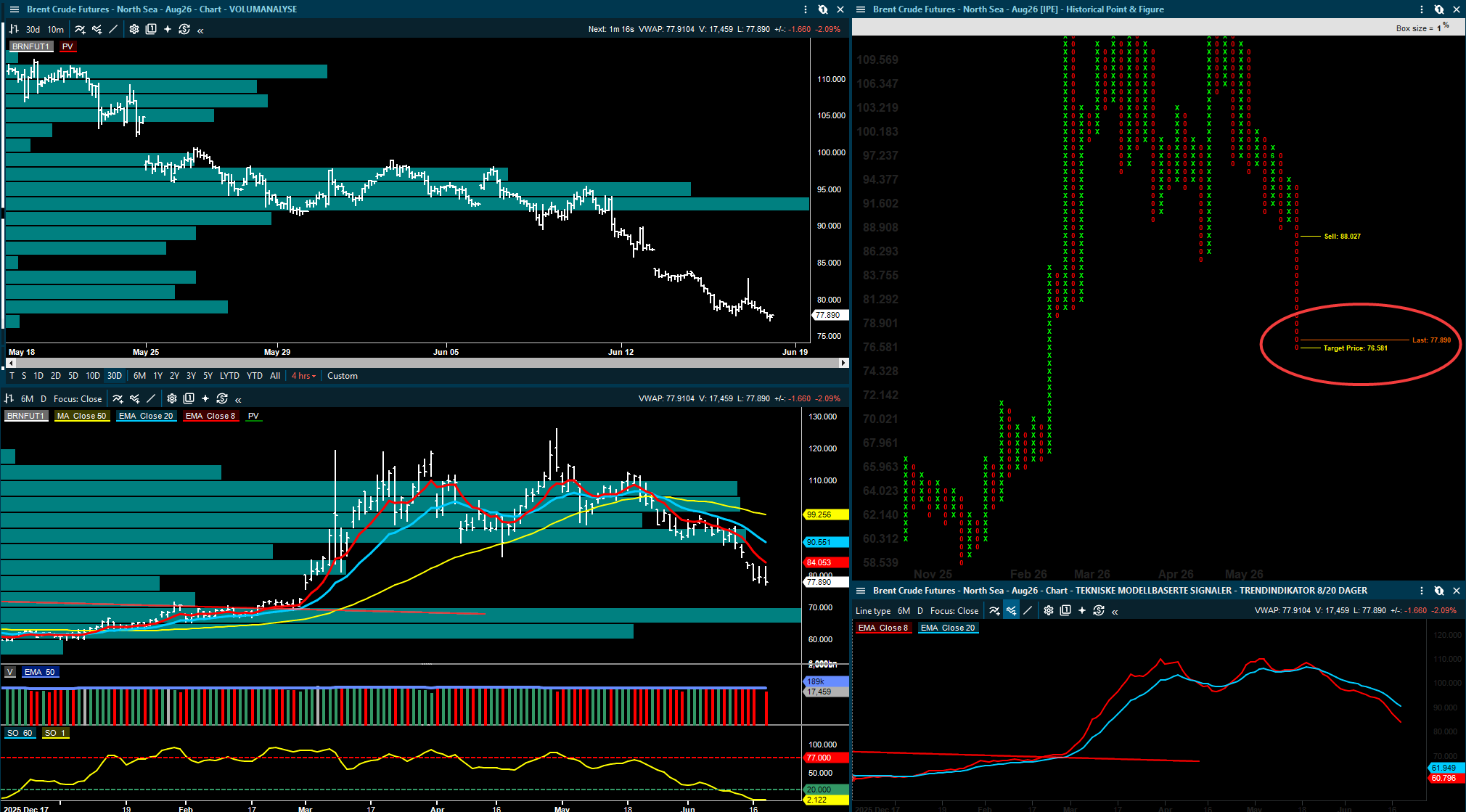

Goldman peker på at den geopolitiske fremdriften ser ut til å ha bremset. Markedet har i en periode priset inn en vei mot mer iransk olje tilbake i markedet, lavere oljepris og mindre inflasjonspress. Det har bidratt til bedre risikovilje.

Men avtalen ser mer komplisert ut enn markedet først antok. USA-Iran-samtalene er utsatt, politiske reiser er utsatt, Israel er misfornøyd, og operasjonene i Libanon er fortsatt et friksjonspunkt. Det gikk over 50 prosjektiler mot israelske styrker i Libanon fra Hezbollah fredag. I tillegg krever Iran mer konkret amerikansk implementering før landet selv går videre.

Det viktigste her er tillit. Dersom Iran gjenoppretter oljeeksporten fullt ut og oljeprisen faller, mister landet sitt viktigste forhandlingskort. Derfor kan en langsommere og mer gradvis implementering være mer rasjonell for Iran enn en rask normalisering.

Markedet har i stor grad priset inn flere fysiske fat olje. Det har ikke nødvendigvis priset inn tillitsproblemet fullt ut.

Hvorfor dette betyr noe for olje, renter og aksjer

Dersom Iran-avtalen går tregere enn ventet, kan oljeprisen få mer støtte enn markedet har lagt til grunn. Da blir inflasjonsrisikoen vanskeligere å avskrive som midlertidig. Dette påvirker rentene, sentralbankforventningene og aksjemarkedet.

Lavere oljepris har vært en viktig del av nøkkelen til markedet. Den gjør det lettere for markedet å tro på lavere inflasjon og mindre behov for stram pengepolitikk. Hvis olje- og geopolitikkrisikoen kommer tilbake, blir denne historien svekket.

Dette er grunnen til at geopolitikk fortsatt er viktig for aksjer, selv om AI dominerer overskriftene. Oljeprisen påvirker inflasjon. Inflasjon påvirker renteforventninger. Renteforventninger påvirker verdsettelsen av vekstaksjer. Og vekstaksjer er igjen kjernen i AI-oppturen.

AI: Kinesisk konkurranse kan øke investeringspresset

En av de mest interessante observasjonene i analysen til Goldman handler om kinesisk AI-konkurranse. Mange har tenkt at billigere modeller og lavere tokenkostnader kan redusere behovet for ekstremt store investeringer. Men Goldman peker på en annen mulig konklusjon: Kinesisk konkurranse kan faktisk øke behovet for å bruke mer penger.

Hvis forspranget mellom amerikanske og kinesiske AI-modeller har krympet fra rundt ett år til kanskje bare noen måneder, endres psykologien hos de store teknologiselskapene. Da blir spørsmålet ikke om man kan spare penger, men om man tør å bruke mindre enn konkurrentene.

I et teknologisk kappløp ønsker ingen å bli frakjørt. Hvis konkurrentene nærmer seg, blir den naturlige reaksjonen ofte å øke tempoet, ikke senke det.

Dette betyr at AI-kappløpet kan bli dyrere og mer intenst enn markedet tidligere har antatt. Og med dyrere så øker risikoen for aksjene.

Hyperscalerne betaler, hardware-selskapene tjener

I denne utviklingen er hyperscalerne finansieringsmotoren. Det er de store teknologiselskapene som Microsoft, Amazon, Alphabet, Meta og andre som må investere enorme beløp i datasentre, strøm, nettverk, chips og infrastruktur.

Hardware-leverandørene er de umiddelbare vinnerne. Halvlederprodusenter, minneselskaper, nettverksleverandører, kjøleleverandører og infrastrukturselskaper får etterspørselen først.

Dette er en viktig forskjell. AI kan være positivt for hele verdikjeden, men kontantstrømmen fordeles ikke likt. De som selger spader i gullrushet får inntektene tidlig. De som bygger selve gullgruvene må bruke kapital først og bevise avkastningen senere.

Markedet liker foreløpig hardware-siden fordi den har tydelige ordre, sterk etterspørsel og synlig kapasitetsmangel. Men for hyperscalerne kan økende AI-investeringer etter hvert bli et spørsmål om kontantstrøm, balanse og kapitalavkastning.

Den tekniske strukturen har vært nesten perfekt

Goldman beskriver uken som nær en perfekt teknisk setup. Sentimentet har vært lavt til moderat, markedsbredden har vært svak, opsjonsforfall har påvirket flyten, og giring har forsterket bevegelsene.

Dette er en viktig kombinasjon. Når sentimentet er svakt, men markedet ikke faller, kan investorer bli tvunget til å kjøpe seg inn igjen. Når opsjonsposisjonering samtidig bidrar til å forsterke bevegelsene, kan markedet bevege seg raskere enn nyhetene alene skulle tilsi.

Det samme som bidro til å akselerere fallet for noen uker siden, virker nå motsatt vei. Mekaniske flows, gamma, opsjoner og trendfølgende strategier kan forsterke oppgangen når markedet først snur opp.

Dette er grunnen til at markedet noen ganger kan virke sterkere enn makrobildet tilsier. Det er ikke bare fundamentale kjøpere som driver kursene. Det er også mekanisk etterspørsel.

Hva betyr CTA-asymmetri til nedsiden?

CTA-er er systematiske trendfølgende fond. De kjøper det som går opp og selger det som går ned, basert på modeller og trendregler. Og det er store fond, som kan påvirke markedet siden de går historisk i flokk.

Når Goldman sier at det nå er mye CTA-asymmetri til nedsiden, betyr det at disse modellene i større grad kan bli selgere dersom markedet begynner å falle. De har trolig økt eksponeringen etter oppgangen, men dersom markedet flater ut eller snur ned, kan modellene raskt redusere risiko.

Dette er viktig fordi CTA-er ikke nødvendigvis vurderer om AI-historien er god eller dårlig. De følger pris og trend. Når trendene peker opp, kan de bidra til kjøpspress. Når trendene svekkes, kan de bidra til salgspress.

Derfor kan markedet bli mer følsomt etter en sterk rekyl. Oppgangen har reparert en del tekniske signaler, men den har også skapt et oppsett hvor systematiske aktører kan bli tvungne selgere ved et brudd ned.

Retail er høyt giret, mens institusjonelle fortsatt er avventende

Et annet viktig signal er forskjellen mellom private og institusjonelle investorer. Goldman peker på at institusjonelt sentiment fortsatt er dempet, selv om fundingindikatorene viser at de har lagt på en del giring mens retail-giring er svært høy.

Dette er interessant markedspsykologi. Private investorer jager i større grad oppsiden, ofte via opsjoner, girede produkter og populære AI-navn. Institusjonelle investorer er mer avventende, men kan bli tvunget til å øke eksponering dersom markedet fortsetter opp.

Dette kan gi støtte på kort sikt. Hvis retail fortsetter å kjøpe, og institusjonelle gradvis må følge etter for ikke å henge etter markedet, kan oppgangen fortsette.

Men det øker også risikoen. Høy retail-giring gjør markedet mer følsomt for raske reverseringer. Dersom AI-navnene faller, kan opsjons- og girede posisjoner raskt gå fra å forsterke oppgangen til å forsterke nedgangen.

Fed er fortsatt vanskelig å avskrive

Selv om AI og geopolitikk dominerer, er Fed fortsatt viktig. Analysen peker på at rentekurven har flatet ut, front-end SOFR-prisingen fortsetter å falle, og enkelte forhold mellom ulike aktivaklasser begynner å bryte ned.

(Front-end SOFR-prising betyr hvordan rentemarkedet priser de korte amerikanske rentene fremover, typisk de neste månedene og de nærmeste 1–2 årene.

SOFR er den amerikanske overnatten-renten som i praksis har erstattet Libor som viktig referanserente. Den ligger tett opp mot det markedet forventer at Fed-renten skal være. Derfor brukes SOFR-futures og SOFR-markedet til å lese hva investorene tror Fed vil gjøre med rentene.

Enkelt forklart:

Når markedet priser lavere front-end SOFR-renter, betyr det at investorene tror Fed etter hvert kan kutte renten eller i hvert fall ikke heve mer.

Når markedet priser høyere front-end SOFR-renter, betyr det at investorene tror Fed må holde renten høyere lenger, eller at risikoen for nye rentehevinger har økt.

Dette betyr at markedet fortsatt prøver å forstå hvordan sentralbanken vil reagere i et miljø hvor inflasjonen ikke er løst, oljeprisen kan svinge, og vekstbildet er ujevnt.

Når Fed gir mindre tydelig fremtidig veiledning, øker usikkerheten. Markedet må i større grad tolke hvert enkelt nøkkeltall, og rentene kan reagere kraftigere på nye data.

Mindre forward guidance betyr ikke nødvendigvis høyere renter, men det betyr ofte mer rentevolatilitet. Og mer rentevolatilitet kan skape mer uro i aksjemarkedet, spesielt i vekstaksjer med høy verdsettelse.

Divergensene bygger seg opp

Goldman analysen peker på flere forhold som ikke helt stemmer med den sterke AI-oppgangen.

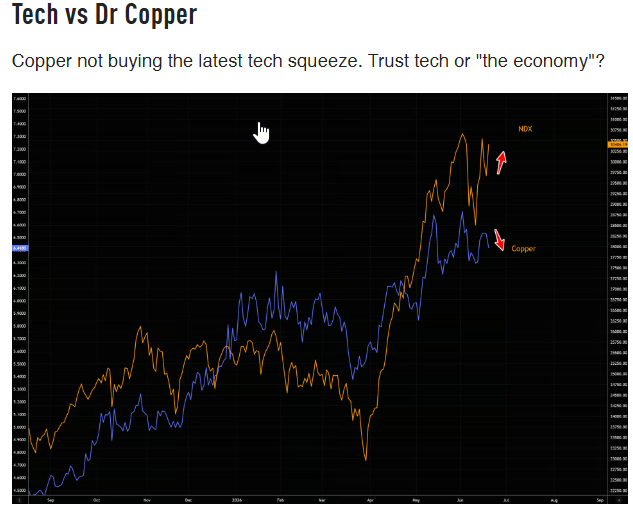

Kobber versus Nasdaq er ett eksempel. Dersom Nasdaq stiger kraftig på AI, men kobber ikke bekrefter den samme vekstoptimismen, kan det bety at teknologimarkedet priser inn en sterk fremtid som realøkonomien ennå ikke bekrefter.

Russell versus SFRZ6 (SOFR futures) er et annet eksempel. Small caps er ofte mer følsomme for renter, kreditt og innenlandsk vekst. Dersom small caps ikke oppfører seg i tråd med renteforventningene, kan det være et tegn på at markedet under overflaten ikke er like sterkt som de store teknologinavnene antyder.

Slike divergenser er viktige fordi de ofte dukker opp før markedet skifter karakter. De betyr ikke nødvendigvis at en vending kommer med en gang, men de forteller at bildet er mindre rent enn indeksene viser.

Markedet har løst én utfordring, men ikke alle

Markedet har klart å kjøpe dippen og løfte AI-lederne til nye høyder. Det viser styrke. Men samtidig er flere risikofaktorer fortsatt til stede.

Geopolitisk momentum er svakere enn markedet har priset inn. AI-kappløpet kan kreve enda større investeringer. CTA-er kan bli selgere dersom markedet snur ned. Retail-giring er høy. Fed-kommunikasjonen kan gi mer rentevolatilitet. Og flere tverrmarkedsforhold gir blandede signaler.

Dette betyr at markedet ikke nødvendigvis er svakt, men det er mer skjørt enn hva overskriftene antyder.

Konklusjon

AI fortsetter å være den dominerende drivkraften i markedet. Investorene kjøper fortsatt de samme temaene: halvledere, minne, strøm, AI-infrastruktur og automatisering. Så lenge disse trendene holder, kan markedet fortsatt presses høyere.

Men oppgangen er smal, og mye av styrken kommer fra tekniske mekanismer, opsjonsflyt, giring og systematiske strategier. Det gjør markedet mer følsomt dersom momentumet snur.

Samtidig er den geopolitiske lettelsen ikke ferdig priset riktig. Markedet forventer mer iransk olje og lavere inflasjonspress, men tillitsproblemet mellom partene kan gjøre implementeringen tregere enn ventet. Hvis olje- og inflasjonsrisikoen kommer tilbake, blir rentebildet igjen viktigere.

Det viktigste poenget er derfor dette:

Markedet er sterkt på overflaten fordi AI fortsatt leder. Men under overflaten er det flere skjøre mekanismer som må følges nøye. Geopolitikk, CTA-posisjonering, retail-giring, Fed-usikkerhet og divergenser mellom teknologi og realøkonomiske signaler gjør at oppgangen ikke bør tolkes som risikofri.

Når en smal AI-ledet oppgang får støtte fra tekniske flows, kan den bli kraftig. Men dersom de samme mekanismene snur, kan bevegelsen også gå raskt motsatt vei.

DISCLAIMER

Denne analysen er kun et utdannings- og treningsverktøy i teknisk analyse, og må ikke tolkes som en individuell anbefaling om handel i finansielle instrumenter.Point & Figure-analysen genererer kjøps- og salgssignaler utelukkende basert på en modell, der signalene beregnes fra kolonner og formasjoners bredde. I chartene fremstår disse som kjøp og salg, men dette er ikke anbefalinger fra Inside Oslo Børs – de er kun resultatet av en objektiv, regelbasert metode. Analysen er uavhengig av tid og fullstendig modellbasert. Innholdet i denne rapporten er kun ment som generell informasjon og opplæring innen teknisk analyse. Eventuelle referanser til kjøp, salg, kursmål eller signaler gjenspeiler objektive modeller som Point & Figure, og skal ikke oppfattes som personlig investeringsråd eller en anbefaling om kjøp eller salg. Taktisk Inside driver ikke porteføljeforvaltning, investeringsrådgivning eller ordreformidling, og omfattes derfor ikke av konsesjonspliktig virksomhet etter verdipapirhandelloven. Investeringer i verdipapirer innebærer alltid risiko, og den enkelte investor er selv ansvarlig for sine beslutninger. Historiske signaler eller modellberegninger er ingen garanti for fremtidig utvikling. Inside Børs og INSIDE TV er redaksjonelle medier. Ansvarlig redaktør: Roger Kristiansen. Alt innhold er analyse og kommentarer, ikke personlig investeringsrådgivning.

Ansvarsfraskrivelse:

Denne teksten er utarbeidet som generell markedsinformasjon og er ikke å anse som investeringsråd. Vurderingene er basert på offentlig tilgjengelig informasjon, teknisk og fundamentale betraktninger og kan endres uten varsel. Historisk utvikling er ingen garanti for fremtidig avkastning.